Ecosyste.ms: Awesome

An open API service indexing awesome lists of open source software.

https://github.com/mschauer/Kalman.jl

Flexible filtering and smoothing in Julia

https://github.com/mschauer/Kalman.jl

filter kalman-filter kalman-smoother tracking

Last synced: about 2 months ago

JSON representation

Flexible filtering and smoothing in Julia

- Host: GitHub

- URL: https://github.com/mschauer/Kalman.jl

- Owner: mschauer

- License: other

- Created: 2018-02-01T09:15:17.000Z (over 6 years ago)

- Default Branch: master

- Last Pushed: 2023-04-19T19:51:12.000Z (about 1 year ago)

- Last Synced: 2024-05-10T16:08:08.899Z (about 2 months ago)

- Topics: filter, kalman-filter, kalman-smoother, tracking

- Language: Julia

- Homepage:

- Size: 692 KB

- Stars: 73

- Watchers: 5

- Forks: 10

- Open Issues: 6

-

Metadata Files:

- Readme: README.md

- License: LICENSE.md

Lists

- awesome-sciml - mschauer/Kalman.jl: Flexible filtering and smoothing in Julia

README

[](https://travis-ci.org/mschauer/Kalman.jl)

[](https://mschauer.github.io/Kalman.jl/latest/)

# Kalman

Flexible filtering and smoothing in Julia. `Kalman` uses [`DynamicIterators`](https://github.com/mschauer/DynamicIterators.jl) (an iterator protocol for dynamic data dependent and controlled processes) and

[`GaussianDistributions`](https://github.com/mschauer/GaussianDistributions.jl) (Gaussian distributions as abstraction for the uncertain state)

to implement flexible online Kalman filtering.

The package provides tools to filter and smooth and conditionally sample the state space system

x[k] = Φx[k−1] + b + w[k], w[k] ∼ N(0, Q)

y[k] = Hx[k] + v[k], v[k] ∼ N(0, R)

## How to use

One way, and maybe *the* way, to use this package is to use `Gaussian` from `GaussianDistributions.jl` as representation of mean and uncertainty of a filter and call `Kalman.correct` to implement the correction step in a Kalman filter:

```julia

using Kalman, GaussianDistributions, LinearAlgebra

using GaussianDistributions: ⊕ # independent sum of Gaussian r.v.

using Statistics

# prior for time 0

x0 = [-1., 1.]

P0 = Matrix(1.0I, 2, 2)

# dynamics

Φ = [0.8 0.2; -0.1 0.8]

b = zeros(2)

Q = [0.2 0.0; 0.0 0.5]

# observation

H = [1.0 0.0]

R = Matrix(0.3I, 1, 1)

# (mock) data

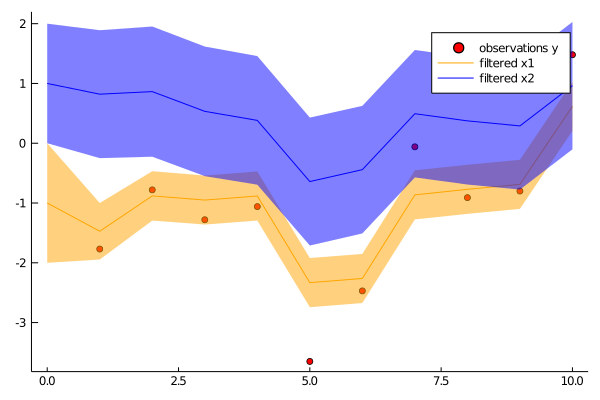

ys = [[-1.77], [-0.78], [-1.28], [-1.06], [-3.65], [-2.47], [-0.06], [-0.91], [-0.80], [1.48]]

# filter (assuming first observation at time 1)

N = length(ys)

p = Gaussian(x0, P0)

ps = [p] # vector of filtered Gaussians

for i in 1:N

global p

# predict

p = Φ*p ⊕ Gaussian(zero(x0), Q) #same as Gaussian(Φ*p.μ, Φ*p.Σ*Φ' + Q)

# correct

p, yres, _ = Kalman.correct(Kalman.JosephForm(), p, (Gaussian(ys[i], R), H))

push!(ps, p) # save filtered density

end

using Plots

p1 = scatter(1:N, first.(ys), color="red", label="observations y")

plot!(p1, 0:N, [mean(p)[1] for p in ps], color="orange", label="filtered x1", grid=false, ribbon=[sqrt(cov(p)[1,1]) for p in ps], fillalpha=.5)

plot!(p1, 0:N, [mean(p)[2] for p in ps], color="blue", label="filtered x2", grid=false, ribbon=[sqrt(cov(p)[2,2]) for p in ps], fillalpha=.5)

savefig(p1, "filter.png")

```

A very similar example of tracking a 2D trajectory can be found [here](example/trajectory_tracking/kalman.jl).

## Interface

The same might be achieved using interface functions

```julia

using DynamicIterators, GaussianDistributions, Kalman, LinearAlgebra

# Define linear evolution

Φ = [0.8 0.5; -0.1 0.8]

b = zeros(2)

Q = [0.2 0.0; 0.0 1.0]

E = LinearEvolution(Φ, Gaussian(b, Q))

# Define observation scheme

H = [1.0 0.0]

R = Matrix(1.0I, 1, 1)

O = LinearObservation(E, H, R)

# Prior

x0 = [1., 0.]

P0 = Matrix(1.0I, 2, 2)

# Observations (mock)

Y = [1 => [1.14326], 2 => [-0.271804], 3 => [-0.00512675]]

# Filter

Xf, ll = kalmanfilter(O, 0 => Gaussian(x0, P0), Y)

@show Xf

```

## Implementation

As said, filtering is implemented via the DynamicIterator protocol. It is worthwhile to look at

a possible the implementation of `kalmanfilter` to see how filtering can be integrated into online algorithms (run in a local scope to avoid `UndefVarError: ystate not defined`.)

```julia

# `Y` is the data iterator, iterating over pairs of `t => v` of time `t` and observation `v`

# `O` is the dynamical filter iterator, iterating over pairs `t => u` where

# u::Tuple{<:Gaussian,<:Gaussian,Float64}

# is the tuple of filtered state, the predicted state and the log likelihood

# Initialise data iterator

ϕ = iterate(Y)

ϕ === nothing && error("no observations")

(t, v), ystate = ϕ

# Initialise dynamical filter with first data point `t => v`

# and the `prior::Pair{Int,<:Gaussian}`, a pair of initial time and initial state

prior = 0 => Gaussian(x0, P0)

ϕ = dyniterate(O, Start(Kalman.Filter(prior, 0.0)), t => v)

ϕ === nothing && error("no observations")

(t, u), state = ϕ

X = [t => u[1]]

while true

# Advance data iterator

ϕ = iterate(Y, ystate)

ϕ === nothing && break

(t, v), ystate = ϕ

# Advance filter with new data `t => v`

ϕ = dyniterate(O, state, t => v)

ϕ === nothing && break

(t, u), state = ϕ

# Do something with the result `t => u` (here: saving it)

push!(X, t => u[1]) # save filtered state

end

ll = u[3] # likelihood

@show X, ll

```