https://github.com/10mohi6/stock-pairs-trading-python

stock-pairs-trading is a python library for backtest with stock pairs trading using kalman filter on Python 3.8 and above.

https://github.com/10mohi6/stock-pairs-trading-python

backtest kalman-filter pairs-trading python stock

Last synced: about 1 year ago

JSON representation

stock-pairs-trading is a python library for backtest with stock pairs trading using kalman filter on Python 3.8 and above.

- Host: GitHub

- URL: https://github.com/10mohi6/stock-pairs-trading-python

- Owner: 10mohi6

- License: mit

- Created: 2022-09-17T12:28:43.000Z (almost 4 years ago)

- Default Branch: main

- Last Pushed: 2023-09-19T11:26:04.000Z (over 2 years ago)

- Last Synced: 2025-04-14T04:14:15.047Z (about 1 year ago)

- Topics: backtest, kalman-filter, pairs-trading, python, stock

- Language: Python

- Homepage:

- Size: 93.8 KB

- Stars: 36

- Watchers: 2

- Forks: 11

- Open Issues: 1

-

Metadata Files:

- Readme: README.md

- License: LICENSE.txt

Awesome Lists containing this project

README

# stock-pairs-trading

[](https://pypi.org/project/stock-pairs-trading/)

[](https://opensource.org/licenses/MIT)

[](https://codecov.io/gh/10mohi6/stock-pairs-trading-python)

[](https://app.travis-ci.com/10mohi6/stock-pairs-trading-python)

[](https://pypi.org/project/stock-pairs-trading/)

[](https://pepy.tech/project/stock-pairs-trading)

stock-pairs-trading is a python library for backtest with stock pairs trading using kalman filter on Python 3.8 and above.

## Installation

$ pip install stock-pairs-trading

## Usage

### find pairs

```python

from stock_pairs_trading import StockPairsTrading

spt = StockPairsTrading(

start="2007-12-01",

end="2017-12-01",

)

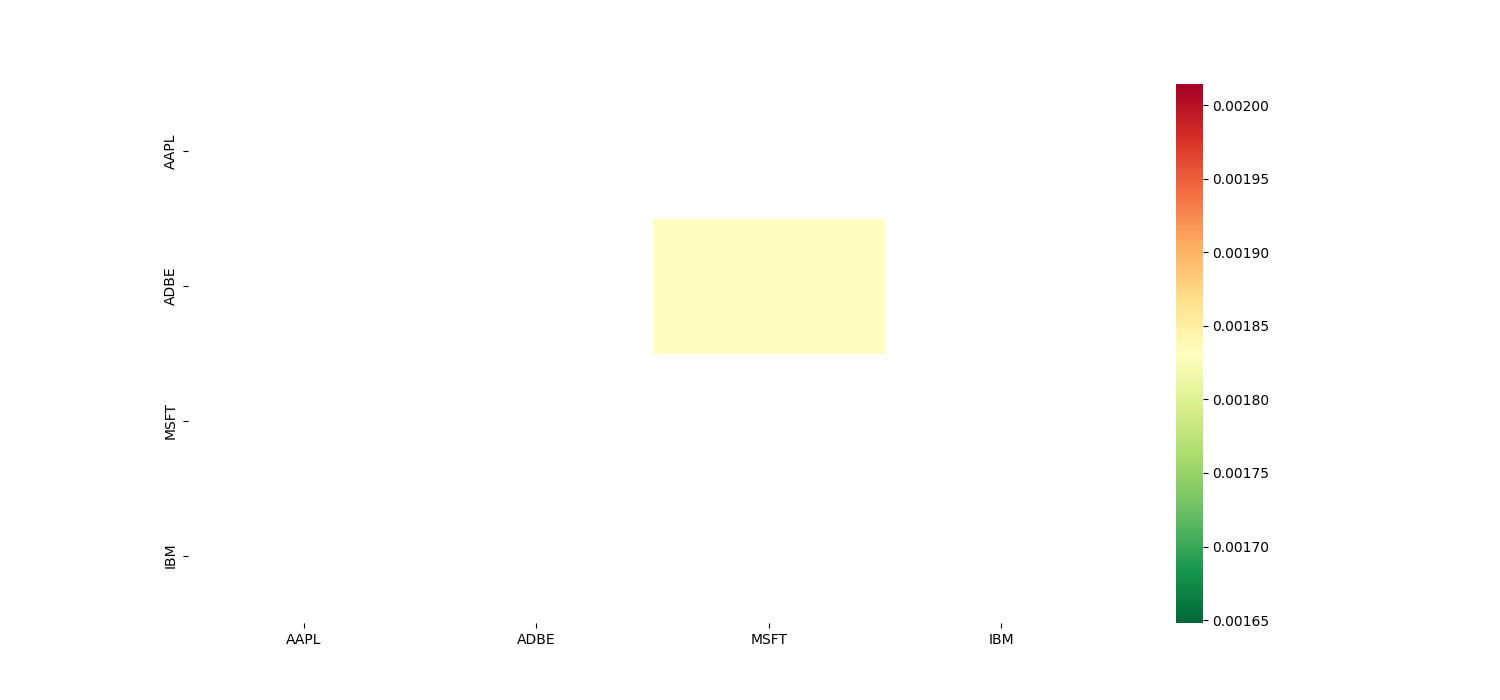

r = spt.find_pairs(["AAPL", "ADBE", "MSFT", "IBM"])

print(r)

```

```python

[('ADBE', 'MSFT')]

```

### backtest

```python

from pprint import pprint

from stock_pairs_trading import StockPairsTrading

spt = StockPairsTrading(

start="2007-12-01",

end="2017-12-01",

)

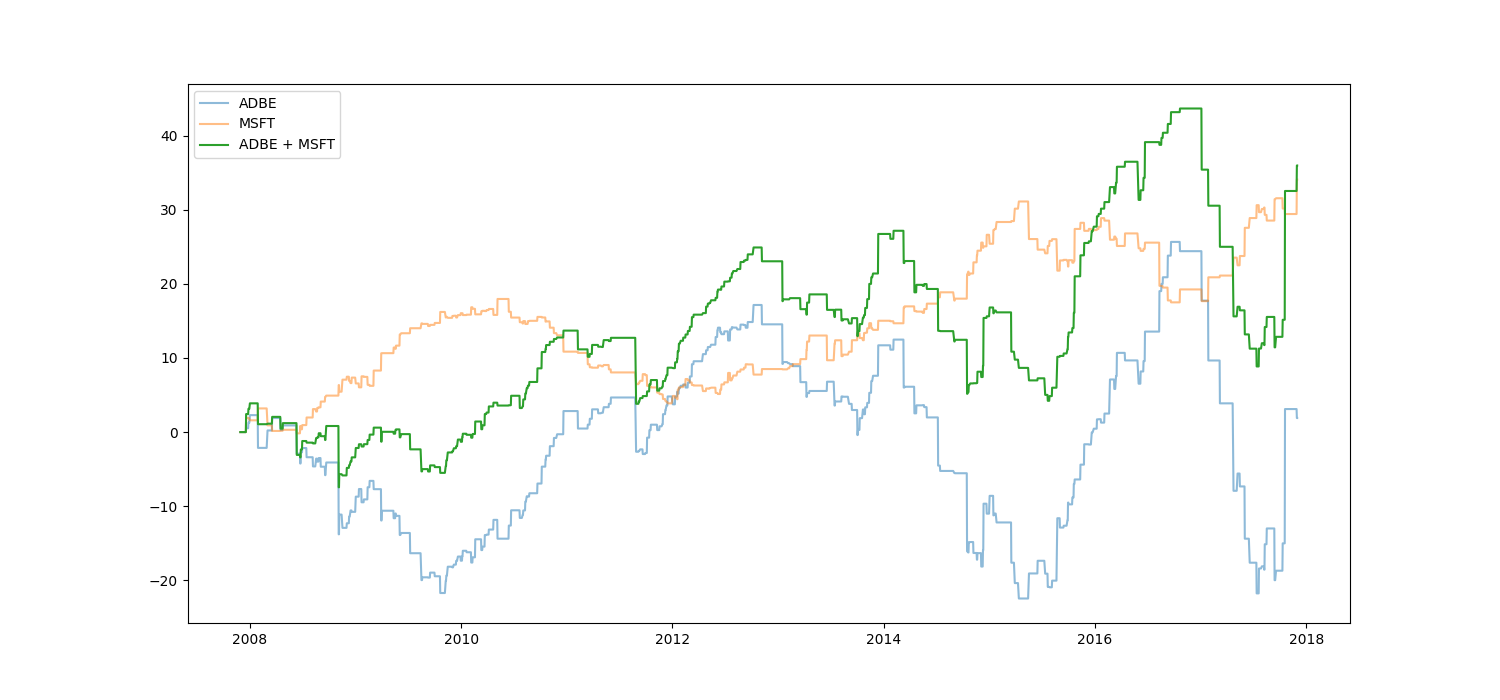

r = spt.backtest(('ADBE', 'MSFT'))

pprint(r)

```

```python

{'cointegration': 0.0018311528816901195,

'correlation': 0.9858057442729853,

'maximum_drawdown': 34.801876068115234,

'profit_factor': 1.1214715644744209,

'riskreward_ratio': 0.8095390763424627,

'sharpe_ratio': 0.03606830691295276,

'total_profit': 35.97085762023926,

'total_trades': 520,

'win_rate': 0.5807692307692308}

```

### latest signal

```python

from pprint import pprint

from stock_pairs_trading import StockPairsTrading

spt = StockPairsTrading(

start="2007-12-01",

end="2017-12-01",

)

r = spt.latest_signal(("ADBE", "MSFT"))

pprint(r)

```

```python

{'ADBE Adj Close': 299.5,

'ADBE Buy': True, # entry buy

'ADBE Cover': False, # exit buy

'ADBE Sell': False, # entry sell

'ADBE Short': False, # exit sell

'MSFT Adj Close': 244.74000549316406,

'MSFT Buy': False, # entry buy

'MSFT Cover': False, # exit buy

'MSFT Sell': True, # entry sell

'MSFT Short': False, # exit sell

'date': '2022-09-16',

'zscore': -36.830427514962274}

```

## Advanced Usage

```python

from pprint import pprint

from stock_pairs_trading import StockPairsTrading

spt = StockPairsTrading(

start="2007-12-01",

end="2017-12-01",

outputs_dir_path = "outputs",

data_dir_path = "data",

column = "Adj Close",

window = 1,

transition_covariance = 0.01,

)

r = spt.backtest(('ADBE', 'MSFT'))

pprint(r)

```