https://github.com/Garve/mamimo

A package to compute a marketing mix model.

https://github.com/Garve/mamimo

Last synced: 5 months ago

JSON representation

A package to compute a marketing mix model.

- Host: GitHub

- URL: https://github.com/Garve/mamimo

- Owner: Garve

- Created: 2022-05-14T22:17:13.000Z (almost 3 years ago)

- Default Branch: main

- Last Pushed: 2023-07-30T08:44:04.000Z (over 1 year ago)

- Last Synced: 2024-10-29T15:31:49.301Z (6 months ago)

- Language: Python

- Size: 170 KB

- Stars: 70

- Watchers: 10

- Forks: 12

- Open Issues: 0

-

Metadata Files:

- Readme: README.md

Awesome Lists containing this project

- awesome-marketing-machine-learning - mamimo

README

# MaMiMo

This is a small library that helps you with your everyday **Ma**rketing **Mi**x **Mo**delling. It contains a few saturation functions, carryovers and some utilities for creating with time features. You can also read my article about it here: [>>>Click<<<](https://towardsdatascience.com/a-small-python-library-for-marketing-mix-modeling-mamimo-100f31666e18).Give it a try via `pip install mamimo`!

# Small Example

You can create a marketing mix model using different components from MaMiMo as well as [scikit-learn](https://scikit-learn.org/stable/). First, we can create a dataset via

```python

from mamimo.datasets import load_fake_mmmdata = load_fake_mmm()

X = data.drop(columns=['Sales'])

y = data['Sales']

````X` contains media spends only now, but you can enrich it with more information.

## Feature Engineering

MaMiMo lets you add time features, for example, via

```python

from mamimo.time_utils import add_time_features, add_date_indicatorsX = (X

.pipe(add_time_features, month=True)

.pipe(add_date_indicators, special_date=["2020-01-05"])

.assign(trend=range(200))

)

```This adds

- a month column (integers between 1 and 12),

- a binary column named special_date that is 1 on the 5h of January 2020 and 0 everywhere else, and

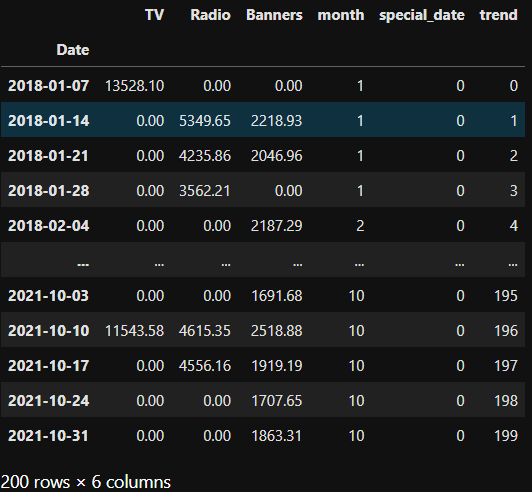

- a (so far linear) trend which is only counting up from 0 to 199.`X` looks like this now:

## Building a Model

We can now build a final model like this:

```python

from mamimo.time_utils import PowerTrend

from mamimo.carryover import ExponentialCarryover

from mamimo.saturation import ExponentialSaturation

from sklearn.linear_model import LinearRegression

from sklearn.preprocessing import OneHotEncoder

from sklearn.compose import ColumnTransformer

from sklearn.pipeline import Pipelinecats = [list(range(1, 13))] # different months, known beforehand

preprocess = ColumnTransformer(

[

('tv_pipe', Pipeline([

('carryover', ExponentialCarryover()),

('saturation', ExponentialSaturation())

]), ['TV']),

('radio_pipe', Pipeline([

('carryover', ExponentialCarryover()),

('saturation', ExponentialSaturation())

]), ['Radio']),

('banners_pipe', Pipeline([

('carryover', ExponentialCarryover()),

('saturation', ExponentialSaturation())

]), ['Banners']),

('month', OneHotEncoder(sparse=False, categories=cats), ['month']),

('trend', PowerTrend(), ['trend']),

('special_date', ExponentialCarryover(), ['special_date'])

]

)model = Pipeline([

('preprocess', preprocess),

('regression', LinearRegression(

positive=True,

fit_intercept=False # no intercept because of the months

)

)

])

```This builds a model that does the following:

- the media channels are preprocessed using the [adstock transformation](https://en.wikipedia.org/wiki/Advertising_adstock), i.e. a carryover effect and a saturation is added

- the month is one-hot (dummy) encoded

- the trend is changed from linear to something like t^a, with some exponent a to be optimized

- the special_date 2020-01-05 gets a carryover effect as well, meaning that not only on this special week there was some special effect on the sales, but also the weeks after it## Training The Model

We can then hyperparameter tune the model via

```python

from scipy.stats import randint, uniform

from sklearn.model_selection import RandomizedSearchCV, TimeSeriesSplittuned_model = RandomizedSearchCV(

model,

param_distributions={

'preprocess__tv_pipe__carryover__window': randint(1, 10),

'preprocess__tv_pipe__carryover__strength': uniform(0, 1),

'preprocess__tv_pipe__saturation__exponent': uniform(0, 1),

'preprocess__radio_pipe__carryover__window': randint(1, 10),

'preprocess__radio_pipe__carryover__strength': uniform(0, 1),

'preprocess__radio_pipe__saturation__exponent': uniform(0, 1),

'preprocess__banners_pipe__carryover__window': randint(1, 10),

'preprocess__banners_pipe__carryover__strength': uniform(0, 1),

'preprocess__banners_pipe__saturation__exponent': uniform(0, 1),

'preprocess__trend__power': uniform(0, 2),

'preprocess__special_date__window': randint(1, 10),

'preprocess__special_date__strength': uniform(0, 1),

},

cv=TimeSeriesSplit(),

random_state=0,

n_iter=1000, # can take some time, lower number for faster results

)tuned_model.fit(X, y)

```You can also use `GridSearch`, Optuna, or other hyperparameter tune methods and packages here, as long as it is compatible to scikit-learn.

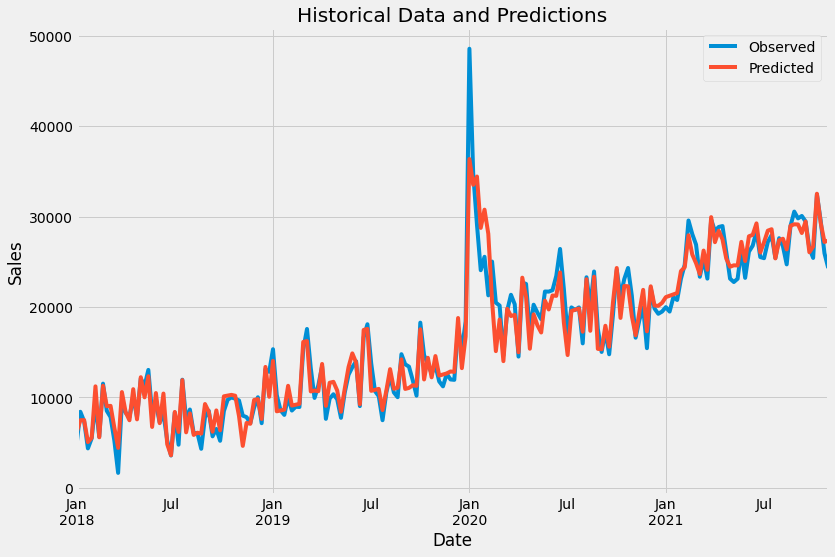

## Analyzing

With `tuned_model.predict(X)` and some plotting, we get

You can get the best found hyperparameters using `print(tuned_model.best_params_)`.

### Plotting

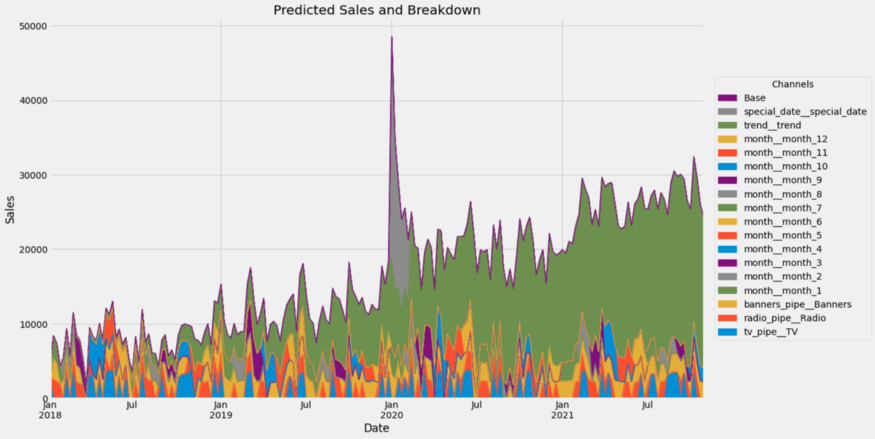

You can compute the channel contributions via

```python

from mamimo.analysis import breakdowncontributions = breakdown(tuned_model.best_estimator_, X, y)

```This returns a dataframe with the contributions of each channel fo each time step, summing to the historical values present in `y`. You can get a nice plot via

```python

ax = contributions.plot.area(

figsize=(16, 10),

linewidth=1,

title="Predicted Sales and Breakdown",

ylabel="Sales",

xlabel="Date",

)

handles, labels = ax.get_legend_handles_labels()

ax.legend(

handles[::-1],

labels[::-1],

title="Channels",

loc="center left",

bbox_to_anchor=(1.01, 0.5),

)

```

Wow, that's a lot of channels. Let us group some of them together.

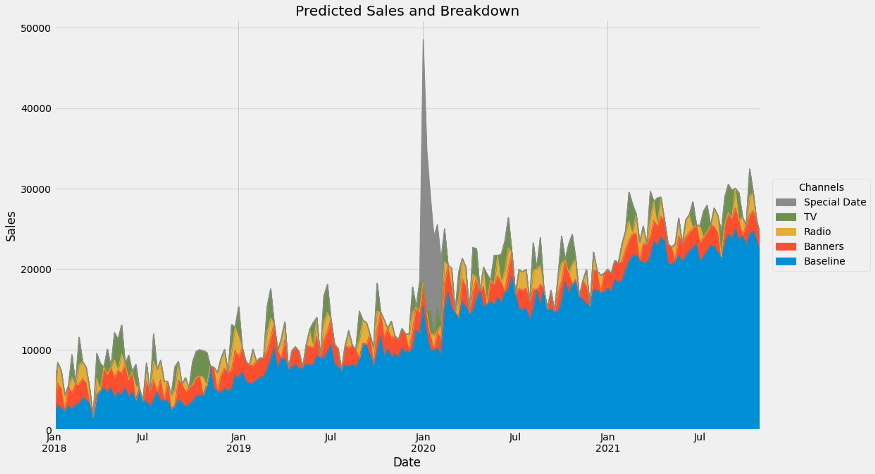

```python

group_channels = {'Baseline': [f'month__month_{i}' for i in range(1, 13)] + ['Base', 'trend__trend']}

# read: 'Baseline consists of the months, base and trend.'

# You can add more groups!contributions = breakdown(

tuned_model.best_estimator_,

X,

y,

group_channels

)

```If we plot again, we get

Yay!

-----------------

[](https://ko-fi.com/G2G7EBKVH)