https://github.com/cerlymarco/tspiral

A python package for time series forecasting with scikit-learn estimators.

https://github.com/cerlymarco/tspiral

autoregressive-forecasters autoregressive-modeling direct-forecasting exogenous-predictors forecasting multivariate-forecasting multivariate-timeseries python recursive-forecasting scikit-learn time-series timeseries timeseries-forecasting

Last synced: over 1 year ago

JSON representation

A python package for time series forecasting with scikit-learn estimators.

- Host: GitHub

- URL: https://github.com/cerlymarco/tspiral

- Owner: cerlymarco

- License: mit

- Created: 2022-07-12T13:07:38.000Z (about 4 years ago)

- Default Branch: main

- Last Pushed: 2024-04-04T14:53:33.000Z (over 2 years ago)

- Last Synced: 2024-10-11T21:43:40.844Z (almost 2 years ago)

- Topics: autoregressive-forecasters, autoregressive-modeling, direct-forecasting, exogenous-predictors, forecasting, multivariate-forecasting, multivariate-timeseries, python, recursive-forecasting, scikit-learn, time-series, timeseries, timeseries-forecasting

- Language: Jupyter Notebook

- Homepage:

- Size: 2.73 MB

- Stars: 160

- Watchers: 6

- Forks: 20

- Open Issues: 0

-

Metadata Files:

- Readme: README.md

- License: LICENSE

Awesome Lists containing this project

README

# tspiral

A python package for time series forecasting with scikit-learn estimators.

tspiral is not a library that works as a wrapper for other tools and methods for time series forecasting. tspiral directly provides scikit-learn estimators for time series forecasting. It leverages the benefit of using scikit-learn syntax and components to easily access the open source ecosystem built on top of the scikit-learn community. It easily maps a complex time series forecasting problems into a tabular supervised regression task, solving it with a standard approach.

## Overview

tspiral provides 4 optimized forecasting techniques:

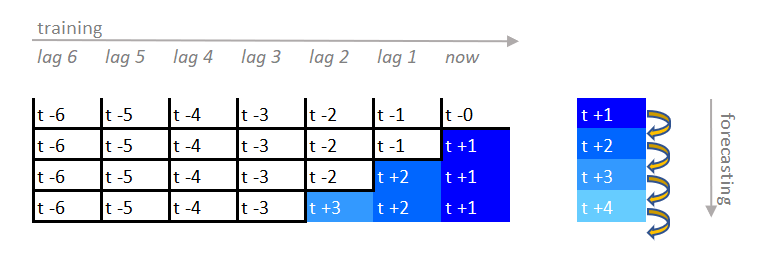

- **Recursive Forecasting**

Lagged target features are combined with exogenous regressors (if provided) and lagged exogenous features (if specified). A scikit-learn compatible regressor is fitted on the whole merged data. The fitted estimator is called iteratively to predict multiple steps ahead.

Which in a compact way we can summarize in:

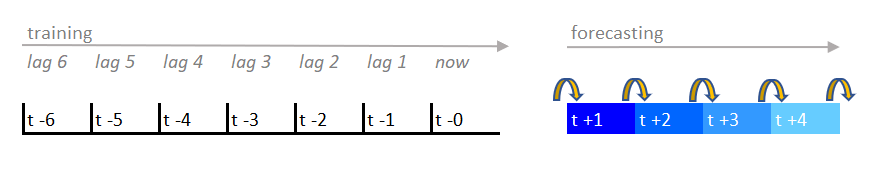

- **Direct Forecasting**

A scikit-learn compatible regressor is fitted on the lagged data for each time step to forecast.

Which in a compact way we can summarize in:

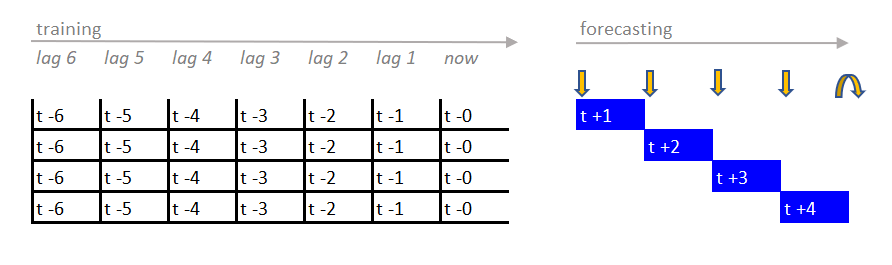

It's also possible to mix recursive and direct forecasting by predicting directly some future horizons while using recursive on the remaining.

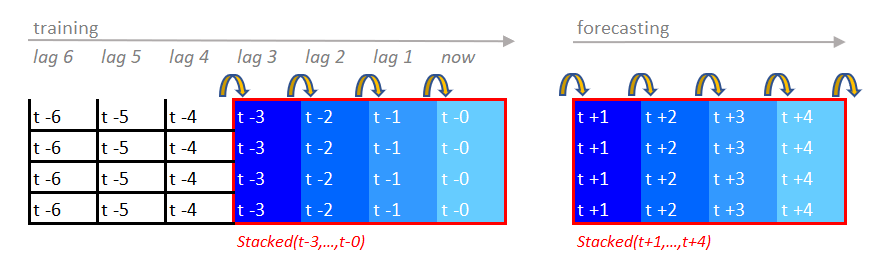

- **Stacking Forecasting**

Multiple recursive time series forecasters are fitted and combined on the final portion of the training data with a meta-learner.

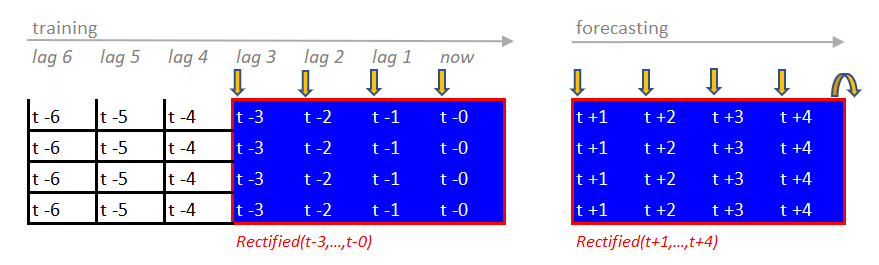

- **Rectified Forecasting**

Multiple direct time series forecasters are fitted and combined on the final portion of the training data with a meta-learner.

**GLOBAL and MULTIVARIATE time series forecasting are natively supported for all the forecasting methods available.** For GLOBAL forecasting, use the `groups` parameter to specify the column of the input data that contains the group identifiers. For MULTIVARIATE forecasting, pass a target with multiple columns when calling fit.

## Installation

```shell

pip install --upgrade tspiral

```

The module depends only on NumPy, Pandas, and Scikit-Learn (>=0.24.2). Python 3.6 or above is supported.

## Media

- [How to Improve Recursive Time Series Forecasting](https://medium.com/towards-data-science/how-to-improve-recursive-time-series-forecasting-ff5b90a98eeb)

- [Time Series Forecasting with Feature Selection: Why you may need it](https://medium.com/towards-data-science/time-series-forecasting-with-feature-selection-why-you-may-need-it-696b23ecc329)

- [Forecast Time Series with Missing Values: Beyond Linear Interpolation](https://medium.com/towards-data-science/forecast-time-series-with-missing-values-beyond-linear-interpolation-2f2adf0a0cba)

- [Time Series Forecasting with Conformal Prediction Intervals: Scikit-Learn is All you Need](https://medium.com/towards-data-science/time-series-forecasting-with-conformal-prediction-intervals-scikit-learn-is-all-you-need-4b68143a027a)

- [Hitting Time Forecasting: The Other Way for Time Series Probabilistic Forecasting](https://medium.com/towards-data-science/hitting-time-forecasting-the-other-way-for-time-series-probabilistic-forecasting-6c3b6496c353)

- [Hitchhiker’s Guide to MLOps for Time Series Forecasting with Sklearn](https://medium.com/towards-data-science/hitchhikers-guide-to-mlops-for-time-series-forecasting-with-sklearn-d5d9728095a7)

## Usage

- **Recursive Forecasting**

```python

import numpy as np

from sklearn.linear_model import Ridge

from tspiral.forecasting import ForecastingCascade

timesteps = 400

e = np.random.normal(0,1, (timesteps,))

y = np.concatenate([

2*np.sin(np.arange(timesteps)*(2*np.pi/24))+e,

2*np.cos(np.arange(timesteps)*(2*np.pi/24))+e,

])

X = [[0]]*timesteps+[[1]]*timesteps

model = ForecastingCascade(

Ridge(),

lags=range(1,24+1),

groups=[0],

).fit(X, y)

forecasts = model.predict([[0]]*80+[[1]]*80)

```

- **Direct Forecasting**

```python

import numpy as np

from sklearn.linear_model import Ridge

from tspiral.forecasting import ForecastingChain

timesteps = 400

e = np.random.normal(0,1, (timesteps,))

y = np.concatenate([

2*np.sin(np.arange(timesteps)*(2*np.pi/24))+e,

2*np.cos(np.arange(timesteps)*(2*np.pi/24))+e,

])

X = [[0]]*timesteps+[[1]]*timesteps

model = ForecastingChain(

Ridge(),

n_estimators=24,

lags=range(1,24+1),

groups=[0],

).fit(X, y)

forecasts = model.predict([[0]]*80+[[1]]*80)

```

- **Stacking Forecasting**

```python

import numpy as np

from sklearn.linear_model import Ridge

from sklearn.tree import DecisionTreeRegressor

from tspiral.forecasting import ForecastingStacked

timesteps = 400

e = np.random.normal(0,1, (timesteps,))

y = np.concatenate([

2*np.sin(np.arange(timesteps)*(2*np.pi/24))+e,

2*np.cos(np.arange(timesteps)*(2*np.pi/24))+e,

])

X = [[0]]*timesteps+[[1]]*timesteps

model = ForecastingStacked(

[Ridge(), DecisionTreeRegressor()],

test_size=24*3,

lags=range(1,24+1),

groups=[0],

).fit(X, y)

forecasts = model.predict([[0]]*80+[[1]]*80)

```

- **Rectified Forecasting**

```python

import numpy as np

from sklearn.linear_model import Ridge

from sklearn.tree import DecisionTreeRegressor

from tspiral.forecasting import ForecastingRectified

timesteps = 400

e = np.random.normal(0,1, (timesteps,))

y = np.concatenate([

2*np.sin(np.arange(timesteps)*(2*np.pi/24))+e,

2*np.cos(np.arange(timesteps)*(2*np.pi/24))+e,

])

X = [[0]]*timesteps+[[1]]*timesteps

model = ForecastingRectified(

[Ridge(), DecisionTreeRegressor()],

n_estimators=24*3,

test_size=24*3,

lags=range(1,24+1),

groups=[0],

).fit(X, y)

forecasts = model.predict([[0]]*80+[[1]]*80)

```

More examples in the [notebooks folder](https://github.com/cerlymarco/tspiral/tree/main/notebooks).