Ecosyste.ms: Awesome

An open API service indexing awesome lists of open source software.

https://github.com/cnelias/serialdependence.jl

Julia module containing standard methods from categorical time-series analysis.

https://github.com/cnelias/serialdependence.jl

categorical-data correlation julia time-series-analysis

Last synced: 2 days ago

JSON representation

Julia module containing standard methods from categorical time-series analysis.

- Host: GitHub

- URL: https://github.com/cnelias/serialdependence.jl

- Owner: CNelias

- License: mit

- Created: 2019-02-01T15:14:06.000Z (almost 6 years ago)

- Default Branch: master

- Last Pushed: 2021-10-08T16:33:39.000Z (about 3 years ago)

- Last Synced: 2024-11-08T11:41:39.553Z (about 2 months ago)

- Topics: categorical-data, correlation, julia, time-series-analysis

- Language: Julia

- Homepage:

- Size: 67.4 KB

- Stars: 3

- Watchers: 2

- Forks: 1

- Open Issues: 0

-

Metadata Files:

- Readme: README.md

- License: LICENSE.md

Awesome Lists containing this project

README

# SerialDependence.jl

When dealing with **categorical data**, things like autocorrelation function are not defined. This is what this module is for : computing **categorical serial dependences**.

|**Travis**|**Appveyor**|

|:--------:|:----------:|

[](https://travis-ci.com/johncwok/SerialDependence.jl)|[](https://ci.appveyor.com/project/johncwok/serialdependence-jl)|

The module mostly implements the methods described in C. Weiss's book *"An Introduction to Discrete-Valued

Time Series"* (2018) [1], with some extras. It contains three main functions :

## Main functions

All the module's functions require a `'lag's` input : `'lags'` can be an `Int`, or an `Array{Int,1}` if you want to do a serial dependence plot. The function then returns a `Float64` or an `Array{Float64,1}` depending on `'lags'` being an `Int` or `Array{Int,1}`.

- **`cramer_coefficient(series, lags)`**: measures average **association** between elements of `'series'` at time `t` and time `t + lags`.

Cramer's k is an *unsigned* measurement : its values lies in [0,1], 0 being perfect independence and 1 perfect dependence. k can be bias, for more infos, refer to [1].

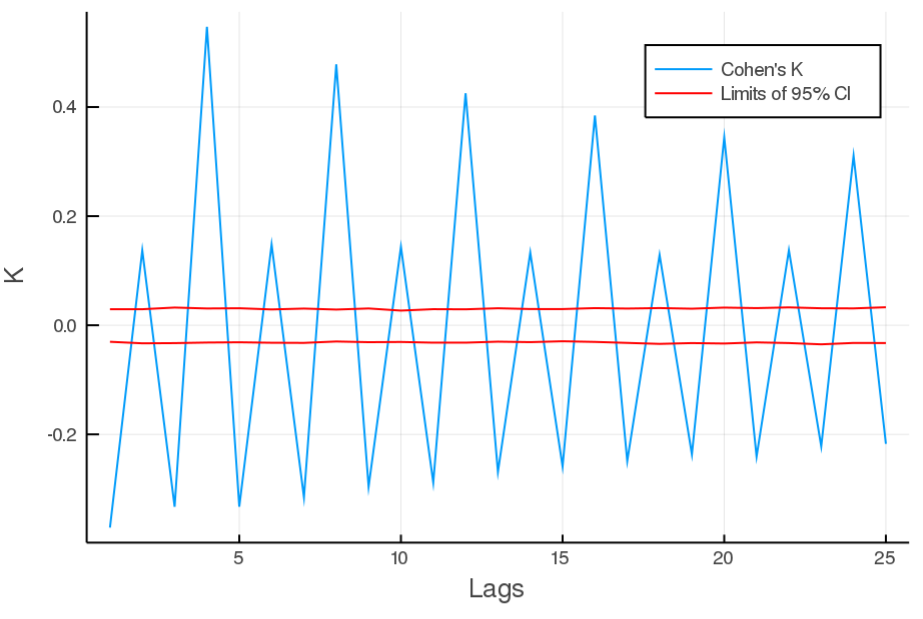

- **`cohen_coefficient(series, lags)`**: measures average **agreement** between elements of `'series'` at time `t` and time `t + lags`.

Cohen's k is a *signed* measurement : its values lie in [-pe/(1 -pe), 1], with positive (negative) values indicating positive (negative) serial dependence at 'lags'. pe is probability of agreement by chance.

- **`theils_u(series, lags)`**: measures average portion of **information** known about `'series'` at `t + lags` given that `'series'` is known at time `t`. U is an *unsigned* measurement: its values lies in [0,1], 0 meaning no information shared and 1 complete knowledge (determinism).

### Usefull extras

- **`bootstrap_CI(Series, lags, coef_func, n_iter = 1000)`**: Returns top and bottom limit for a 95% confidence interval at values of 'lags'.

* `'coef_func'` is the **function** for which the CI needs to be computed. Possible values : 'cramer_coefficient, cohen_coefficient, theils_u'.

* `'n_iter'` controls how many iterations are run during the bootstrap process. Large `'n_iter'`, means more precision but also more compute time.

- **`rate_evolution(Series)`**: This is a visual test of "stationarity" : if it varies linearly, then the time-series can be considered as stationary. Returns an `array` of `array`. Each of the internal array represents one of the categories in `'Series'`and describes it's evolution rate.

## Example

Using the pewee birdsong data (1943) one can do a serial dependence plot using Cohen's cofficient as follow :

```Julia

using DelimitedFiles

using SerialDependence

using Plots

#reading 'pewee' time-series test folder.

series = readdlm("test\\pewee.txt",',')[1,:]

lags = collect(1:25)

v = cohen_coefficient(series, lags)

t, b = bootstrap_CI(series, cramer_coefficient, lags)

a = plot(lags, v, xlabel = "Lags", ylabel = "K", label = "Cramer's k")

plot!(a, lags, t, color = "red", label = "Limits of 95% CI"); plot!(a, lags, b, color = "red", label = "")

```

## TO-DO

[] Implement bias correction for cramer's v

[1] DOI : 10.1002/9781119097013