https://github.com/imann128/tsauditor

A data quality auditing library for time-series tabular data in financial and sensor domains.

https://github.com/imann128/tsauditor

anomaly-detection chronological-data eda financial-analysis leakage-detection sensor-analysis sensor-data time-series time-series-analysis

Last synced: 12 days ago

JSON representation

A data quality auditing library for time-series tabular data in financial and sensor domains.

- Host: GitHub

- URL: https://github.com/imann128/tsauditor

- Owner: imann128

- License: mit

- Created: 2026-05-22T14:23:08.000Z (about 2 months ago)

- Default Branch: main

- Last Pushed: 2026-06-30T09:01:28.000Z (17 days ago)

- Last Synced: 2026-06-30T11:04:49.170Z (17 days ago)

- Topics: anomaly-detection, chronological-data, eda, financial-analysis, leakage-detection, sensor-analysis, sensor-data, time-series, time-series-analysis

- Language: Python

- Homepage:

- Size: 876 KB

- Stars: 8

- Watchers: 1

- Forks: 2

- Open Issues: 9

-

Metadata Files:

- Readme: README.md

- Changelog: CHANGELOG.md

- Contributing: CONTRIBUTING.md

- License: LICENSE

Awesome Lists containing this project

README

# tsauditor

[](https://github.com/imann128/tsauditor/actions/workflows/ci.yml)

[](https://codecov.io/github/imann128/tsauditor)

[](LICENSE)

A data-quality auditing library for **time-series tabular data**, with a focus on

financial and sensor domains. `tsauditor` scans a `DataFrame` and returns a

structured report of structural problems, anomalies, and — its core contribution —

**data-leakage** between features and the prediction target. It can also *repair*

the flagged issues on a copy, score data health, export a formal report, and hand

a clean array straight to a forecasting model.

The project grew out of a real bug in a Pakistani equity (OGDC) direction-prediction

model: a same-day percentage-change feature (`ChangeP`) was mathematically near-identical

to the target it was meant to predict. With `ChangeP` included, a Random Forest

classifier reached 99.68% accuracy (AUC 0.9987); a Gradient Boosting classifier reached

the same 99.68% accuracy (AUC 0.9967). Removing it — along with same-day `Open`, `High`,

and `Low`, which are equally unavailable at prediction time — dropped accuracy to 69.81%

(RF, AUC 0.7795) and 73.70% (GBM, AUC 0.8072) on a held-out test period

(2025-01-09 to 2026-04-03). Both models still beat a 50% baseline, but the headline

accuracy had been almost entirely an artifact of the leak. `tsauditor` exists to catch

this class of mistake automatically before it reaches a model.

See [`examples/ogdc_leakage_case`](examples/ogdc_leakage_case) for the full experiment,

script, and measured results.

## Not just price and direction

`tsauditor` is **column-agnostic** — it never hard-codes `price`, `Direction`, or any

other column. `price`/`Direction` are simply the columns in the OGDC example above. The

structural (PRF), anomaly (ANO), and target-relative leakage (LEK001–003) checks apply to

*any* numeric time-series column. Version 0.2.0 adds two **declarative** mechanisms —

`available_at=` (point-in-time release correctness) and `constraints=` (domain validity) —

so you can also audit macro, sentiment, order-book, volatility, and other alternative-data

columns correctly. tsauditor never *computes* these features; you point it at your columns

and, where relevant, declare their semantics.

| Column type | What can go wrong | Check |

|-------------|-------------------|-------|

| Macro indicators (CPI, rates, unemployment) | Published weeks after their reference date → used early | LEK004 as-of (`available_at=`) |

| Sentiment scores (news / social) | Publish lag; also must sit in a bounded range | LEK004 + VAL001 bounds |

| Order book (bid, ask) | Crossed book (`ask < bid`) | VAL002 relation |

| Bid-ask spread | Zero or negative spread | VAL001 strict-positive bound |

| Volume | Negative volume (feed glitch) | VAL001 non-negative bound |

| Bounded indicators (RSI 0–100, probabilities, ratios) | Out-of-range values | VAL001 bounds |

| Realized volatility / drawdown | Impossible negatives | VAL001 non-negative bound |

| OHLC bars | `Low > High`, `Open`/`Close` outside `[Low, High]` | VAL002 relations |

| Earnings / fundamentals | Point-in-time restatement / release lag | LEK004 as-of |

| Any numeric series | Gaps, stuck runs, outliers, non-stationarity, target leakage | PRF / ANO / LEK001–003 |

See [`examples/beyond_price_direction`](examples/beyond_price_direction) (validity on real

volume/RSI/OHLC columns) and

[`examples/new_features_walkthrough.ipynb`](examples/new_features_walkthrough.ipynb)

(as-of leakage, sentiment bounds).

## Installation

```bash

pip install tsauditor

```

Requires Python ≥ 3.9. Core dependencies: `pandas`, `numpy`, `scipy`, `statsmodels`, `rich`.

Optional extras (install only what you need):

```bash

pip install 'tsauditor[pdf]' # PDF report export (matplotlib)

pip install 'tsauditor[polars]' # polars DataFrame input

pip install 'tsauditor[dev]' # test + lint toolchain (contributors)

```

### Development setup

```bash

git clone https://github.com/imann128/tsauditor.git

cd tsauditor

pip install -e ".[dev]"

```

## **Note:** Set domain="None" for domain agnostic usage. Similarly, it works well without defining a domain at all.

**For usage snippets, scroll down in the readme or check out the [examples](./examples) directory for sample scripts and notebooks.**

## Quickstart

```python

import tsauditor as tsa

report = tsa.scan(df, target="Direction", domain="finance")

report.summary() # rich-formatted CLI table

report.critical # list[Issue] that block modeling

report.filter(module="leakage") # programmatic filtering

report.leaky_columns() # the shortlist of features to review/remove

report.to_json("report.json") # structured export

# Repair on a copy and keep the audit trail (original is never modified):

clean, report = tsa.fix(df, target="Direction", domain="finance")

print(report.last_fixes) # exactly what changed

```

`scan()` returns a `GuardReport` holding `Issue` dataclasses bucketed by severity

(`critical`, `warnings`, `info`) plus dataset metadata.

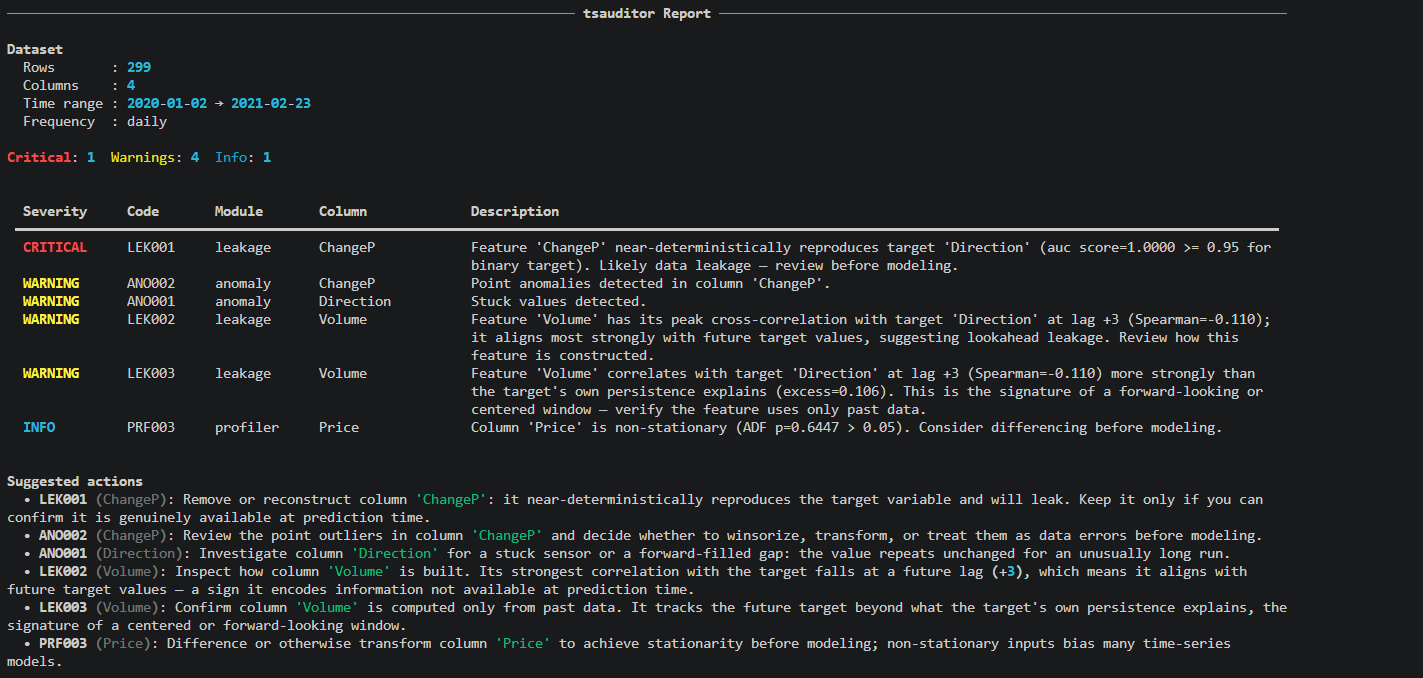

### Example report

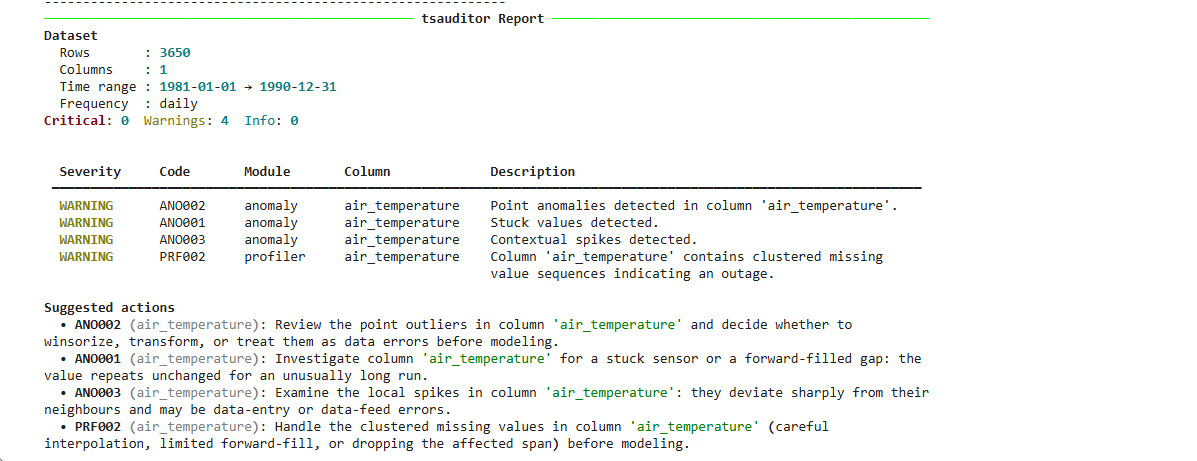

## Sensor:

### Real-World Sensor Validation Example

Below is an example using real weather station telemetry data. To showcase how `tsauditor` behaves during typical field failures, we manually inject three classic hardware faults: a frozen sensor reading, a complete network dropout gap, and a high-voltage electrical spike.

```python

import pandas as pd

import tsauditor as tsa

print(" Fetching real-world weather station sensor dataset...")

url = "[https://raw.githubusercontent.com/jbrownlee/Datasets/master/daily-min-temperatures.csv](https://raw.githubusercontent.com/jbrownlee/Datasets/master/daily-min-temperatures.csv)"

try:

df = pd.read_csv(url, parse_dates=["Date"], index_col="Date")

df.columns = ["air_temperature"]

print(" Dataset successfully into memory")

except Exception as e:

print(f" Error loading dataset: {e}")

print(" Injecting typical hardware field failures for evaluation...")

# 1. Stuck sensor condition: flatlined at 12.2°C for 15 days straight

df.iloc[100:115] = 12.2

# 2. Transmission blackout: 10 days of completely missing telemetry

df.iloc[300:310] = None

# 3. Electrical surge: an impossible 75°C transient spike

df.iloc[500] = 75.0

print("\n Running `tsauditor` validation sweep")

# Execute the audit using the optimized sensor preset

report = tsa.scan(df, domain="sensor")

report.summary()

```

### Example output

## What it checks

| Module | Code | Severity | Detects |

|--------|------|----------|---------|

| profiler | PRF001 | warning | Irregular timestamp frequency |

| profiler | PRF002 | warning | Clustered missing values |

| profiler | PRF003 | info | Non-stationarity (Augmented Dickey-Fuller) |

| profiler | PRF004 | critical | Duplicate timestamps |

| profiler | PRF005 | warning | Clustered gaps |

| profiler | PRF006 | warning | High overall missing rate |

| anomaly | ANO001 | warning | Stuck / repeated constant values |

| anomaly | ANO002 | warning | Point outliers (z-score + IQR) |

| anomaly | ANO003 | warning | Contextual spikes (local rolling z-score) |

| leakage | LEK001 | critical | Target equivalence (feature reproduces the target) |

| leakage | LEK002 | warning | Positive-lag cross-correlation peak (future info) |

| leakage | LEK003 | warning | Rolling-window lookahead (excess over persistence) |

| leakage | LEK004 | critical | As-of leakage (value used before its release time) |

| validity | VAL001 | warning | Out-of-range value (declared per-column bounds) |

| validity | VAL002 | critical | Ordering violation (e.g. crossed book, `bid > ask`) |

Codes marked **critical** block modeling; **warning** and **info** are advisory.

### Leakage detection (the research core)

Leakage checks are **rank-based**, chosen by target type:

- **LEK001 — equivalence.** Continuous targets use `|Spearman ρ|`; binary targets use

**AUC separation** (`max(AUC, 1−AUC)`). This is deliberate: Pearson against a binary

0/1 target is point-biserial correlation, which is capped near `√(2/π) ≈ 0.798`, so a

feature whose sign *defines* the target scores only ~0.80 and slips under a naive

threshold. AUC scores it 1.0.

- **LEK002 — cross-correlation.** Flags features whose peak association with the target

falls at a *positive* lag (the feature aligns with the target's future).

- **LEK003 — temporal lookahead.** Flags features that correlate with the future target

*beyond* what the target's own autocorrelation can explain — the signature of a

forward-looking or centered window. The persistence baseline is what keeps a

legitimate trailing feature from being false-flagged.

- **LEK004 — as-of / point-in-time.** Flags a feature whose value sits at a timestamp

*earlier* than when it was actually published — the classic macro/sentiment trap. See

[As-of leakage](#as-of-leakage-point-in-time) below.

LEK002/LEK003 are WARNING-level *suspicions*: in pure cross-correlation a genuine strong

predictor and a leak are distinguishable only by magnitude. LEK001 and LEK004 are CRITICAL

because equivalence and confirmed availability violations are near-deterministic.

### As-of leakage (point-in-time)

Macro releases (CPI, rates, unemployment), earnings, and news/social sentiment describe a

*reference period* but are only published later. A value aligned to its reference date and

used on that date leaks the future. This cannot be inferred from values alone, so LEK004 is

**opt-in**: you declare when each value became available.

```python

import pandas as pd

# CPI for a reference month is released ~30 days later:

report = tsa.scan(df, available_at={"cpi": pd.Timedelta(days=30)})

# Or, for a ragged real release calendar, pass per-row publish timestamps:

report = tsa.scan(df, available_at={"cpi": publish_times}) # a pd.Series on df.index

```

The fix LEK004 suggests is not to drop the column but to **shift it to its release

schedule** so each value is only used on or after publication.

### Validity checks (domain constraints)

Some values are not merely surprising, they are *impossible*: a non-positive bid-ask

spread, a sentiment score outside `[-1, 1]`, a crossed order book. tsauditor can't guess

these rules, so you declare them via `constraints`:

```python

report = tsa.scan(

df,

constraints={

"bounds": {

"spread": {"min": 0, "min_exclusive": True}, # strictly positive

"sentiment": {"min": -1, "max": 1},

},

"relations": [("bid", "ask")], # bid <= ask must hold every row

},

)

```

`bounds` violations raise **VAL001** (WARNING); a broken `relations` ordering (a crossed

book) raises **VAL002** (CRITICAL). Validity issues are data errors, so they are *not*

counted as leakage in `leaky_columns()`.

## Repair & remediation

tsauditor is advisory by default — it reports and suggests, but only edits your data when

you ask. Every repair happens on a **copy**; your original frame is your backup.

```python

# Advisory only:

report.suggestions() # per-issue suggested action, ordered by severity

# One-shot scan + repair, returning both the clean copy and the report:

clean, report = tsa.fix(df, target="Direction", domain="finance")

# Or repair from an existing report with fine-grained control:

clean = report.apply_fixes(

df,

missing="interpolate", # impute clustered-missing + anything NaN-ed below

outliers="clip", # winsorize ANO002 points / ANO003 spikes ("nan" to drop-to-NaN)

stuck="nan", # replace stuck runs with NaN, then impute

leakage=None, # "drop" to remove leaky columns (off by default)

)

print(report.last_fixes) # structured change log: column, action, cells changed

```

Repairs are **report-driven** (only flagged columns are touched), **time-series safe**

(an outlier is set to NaN and imputed, never deleted — deleting rows would break the

index), and the **target label is never repaired** (interpolating a 0/1 label into

fractions is always wrong).

### Data Health Score

```python

report.health_score(df) # % of numeric cells NOT implicated by a quality issue

```

`100 × (1 − affected_cells / total_cells)`, leakage excluded (a leaky column is a modeling

risk, not corrupt data). It re-scans the frame you pass, so calling it on a `fix()` output

gives a true "after" score.

## Export (JSON + PDF)

```python

report.to_json("report.json", df=df, fixed_df=clean) # includes health + before/after

report.to_pdf("report.pdf", df=df, fixed_df=clean) # needs 'tsauditor[pdf]'

```

`to_pdf` produces a formal, vector, text-selectable report (Times New Roman, black text,

headings and tables — no charts, no colour coding): a Data Health Scorecard, dataset

overview, before/after comparison, target-leakage callout, executive summary, and a

paginated issues table.

## Feeding a forecasting model (TimesFM adapter)

Zero-shot forecasters such as Google TimesFM tokenize a clean, contiguous, finite context

window; a raw series with gaps fails tokenization. The adapter audits, repairs, and returns

a plain `float32` array — and **verifies it is finite** before returning, so a NaN never

reaches the model. It adds no `timesfm` dependency.

```python

array = tsa.adapters.to_timesfm(df, target_col="close_price", domain="finance")

# array is now safe to pass to model.forecast(inputs=[array], ...)

# keep the audit trail too:

array, report = tsa.adapters.to_timesfm(df, target_col="close_price", return_report=True)

```

`context_len` / `min_context` are your knobs, not TimesFM constants — TimesFM 2.5 accepts a

wide range of context lengths (up to 16k). See

[`examples/timesfm_adapter`](examples/timesfm_adapter) for a full walkthrough — the

finiteness guard, context truncation, and the model call.

## Architecture

```

tsauditor/

├── scanner.py # scan() — orchestrates all modules into a GuardReport

├── profiler/ # structural checks: frequency, missing, stationarity

├── anomaly/ # point.py, contextual.py

├── leakage/ # equivalence.py, correlation.py, temporal.py, asof.py

├── validity.py # domain-constraint checks (bounds + relations)

├── remediate.py # apply_fixes / fix engine, health score (repair on a copy)

├── adapters/ # boundary adapters (e.g. timesfm.py)

├── report/

│ ├── summary.py # GuardReport + Issue dataclasses, rich/JSON output

│ ├── remediation.py # code -> suggested-action advisory lookup

│ └── pdf.py # to_pdf export

└── utils/validation.py # input validation & DataFrame normalization

```

## Scaling

**polars input.** A polars `DataFrame` works anywhere a pandas one does — just name

the datetime column via `time_col` (polars has no index):

```python

report = tsa.scan(pl_df, target="Direction", time_col="Date", domain="finance")

```

Install with `pip install 'tsauditor[polars]'`. tsauditor converts to pandas at the

boundary; the audit logic is identical. (See issue #28.)

**Audit a whole universe in parallel.** `scan()` is a pure function and `GuardReport`

is a plain, picklable dataclass, so it parallelises cleanly with `joblib` — ideal for

sweeping every symbol for leakage before you train:

```python

from joblib import Parallel, delayed

import tsauditor as tsa

def audit(symbol, df):

return symbol, tsa.scan(df, target="Direction", domain="finance")

reports = dict(Parallel(n_jobs=-1)(

delayed(audit)(sym, frames[sym]) for sym in frames

))

# every symbol whose feature set leaks into the target

leaky = {s: r.leaky_columns() for s, r in reports.items() if r.leaky_columns()}

```

**Skip the expensive check.** The ADF stationarity test (PRF003) dominates runtime;

`scan(run_stationarity=False)` skips it for a much faster structural/anomaly/leakage sweep.

## Examples

Run `pip install -e ".[dev,examples]"` for running all example notebooks easily.

See [`examples/`](examples) (indexed in [`examples/README.md`](examples/README.md)):

- `ogdc_leakage_case/` — the flagship LEK001 case on real OGDC data (script + notebook).

- `beyond_price_direction/` — validity (VAL001/VAL002) on real volume, RSI, and OHLC

columns: concrete proof tsauditor audits more than price and direction.

- `timesfm_adapter/` — the messy-data -> finite float32 array bridge for Google TimesFM

(finiteness guard, context truncation).

- `sensor-example/` — structural/anomaly checks on a sensor stream, plus a PDF-report demo.

- `new_features_walkthrough.ipynb` — LEK004, validity checks, `tsa.fix`, and the TimesFM

adapter, end-to-end.

- `validation_comparison/` — time-series validation vs general profiling.

## Testing

```bash

pytest -q

```

## Contributing

Contributions are welcome. Check [open issues](https://github.com/imann128/tsauditor/issues)

for ideas, or look for the `good first issue` label. Run `pytest -q` before opening a PR —

the full suite (164 tests) must pass, and CI will verify this across

Python 3.9–3.14 on Linux, Windows, and macOS. See [CONTRIBUTING.md](CONTRIBUTING.md).

## Featured On:

Featured #7 on [Data Science Weekly Issue - 657](https://datascienceweekly.substack.com/p/data-science-weekly-issue-657)

[Article about tsauditor on LineUp Digest](https://lineupdigest.com/en/article/poka-vse-molcat-tsauditor-meniaet-podxod-k-upravleniiu-time-series-dannymi)

## Status

Beta (`0.2.0`). Profiler, anomaly, leakage, validity, remediation, and export modules are

implemented and tested (164 tests passing; CI across Python 3.9–3.14 on

Linux, Windows, macOS).

## License

MIT — see [LICENSE](LICENSE).