https://github.com/probml/dynamax

A Python package for probabilistic state space modeling with JAX

https://github.com/probml/dynamax

hidden-markov-models jax kalman-filter python state-space-models

Last synced: about 1 year ago

JSON representation

A Python package for probabilistic state space modeling with JAX

- Host: GitHub

- URL: https://github.com/probml/dynamax

- Owner: probml

- License: mit

- Created: 2022-04-11T23:42:29.000Z (over 4 years ago)

- Default Branch: main

- Last Pushed: 2025-05-10T11:24:18.000Z (about 1 year ago)

- Last Synced: 2025-05-10T11:35:45.980Z (about 1 year ago)

- Topics: hidden-markov-models, jax, kalman-filter, python, state-space-models

- Language: Python

- Homepage: https://probml.github.io/dynamax/

- Size: 241 MB

- Stars: 815

- Watchers: 25

- Forks: 94

- Open Issues: 56

-

Metadata Files:

- Readme: README.md

- Contributing: CONTRIBUTING.md

- License: LICENSE

- Citation: CITATION.cff

Awesome Lists containing this project

- awesome-jax - dynamax - State Space Models library in JAX. <img src="https://img.shields.io/github/stars/probml/dynamax?style=social" align="center"> (Libraries)

- awesome-jax - Dynamax - Probabilistic state space models. <img src="https://img.shields.io/github/stars/probml/dynamax?style=social" align="center"> (Libraries)

README

# Welcome to DYNAMAX!

[](https://doi.org/10.21105/joss.07069)

Dynamax is a library for probabilistic state space models (SSMs) written

in [JAX](https://github.com/google/jax). It has code for inference

(state estimation) and learning (parameter estimation) in a variety of

SSMs, including:

- Hidden Markov Models (HMMs)

- Linear Gaussian State Space Models (aka Linear Dynamical Systems)

- Nonlinear Gaussian State Space Models

- Generalized Gaussian State Space Models (with non-Gaussian emission

models)

The library consists of a set of core, functionally pure, low-level

inference algorithms, as well as a set of model classes which provide a

more user-friendly, object-oriented interface. It is compatible with

other libraries in the JAX ecosystem, such as

[optax](https://github.com/deepmind/optax) (used for estimating

parameters using stochastic gradient descent), and

[Blackjax](https://github.com/blackjax-devs/blackjax) (used for

computing the parameter posterior using Hamiltonian Monte Carlo (HMC) or

sequential Monte Carlo (SMC)).

## Documentation

For tutorials and API documentation, see: https://probml.github.io/dynamax/.

For an extension of dynamax that supports structural time series models,

see https://github.com/probml/sts-jax.

For an illustration of how to use dynamax inside of [bayeux](https://jax-ml.github.io/bayeux/) to perform Bayesian inference

for the parameters of an SSM, see https://jax-ml.github.io/bayeux/examples/dynamax_and_bayeux/.

## Installation and Testing

To install the latest releast of dynamax from PyPi:

``` {.console}

pip install dynamax # Install dynamax and core dependencies, or

pip install dynamax[notebooks] # Install with demo notebook dependencies

```

To install the latest development branch:

``` {.console}

pip install git+https://github.com/probml/dynamax.git

```

Finally, if you\'re a developer, you can install dynamax along with the

test and documentation dependencies with:

``` {.console}

git clone git@github.com:probml/dynamax.git

cd dynamax

pip install -e '.[dev]'

```

To run the tests:

``` {.console}

pytest dynamax # Run all tests

pytest dynamax/hmm/inference_test.py # Run a specific test

pytest -k lgssm # Run tests with lgssm in the name

```

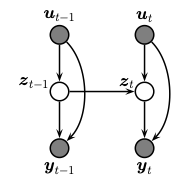

## What are state space models?

A state space model or SSM is a partially observed Markov model, in

which the hidden state, $z_t$, evolves over time according to a Markov

process, possibly conditional on external inputs / controls /

covariates, $u_t$, and generates an observation, $y_t$. This is

illustrated in the graphical model below.

The corresponding joint distribution has the following form (in dynamax,

we restrict attention to discrete time systems):

$$p(y_{1:T}, z_{1:T} \mid u_{1:T}) = p(z_1 \mid u_1) \prod_{t=2}^T p(z_t \mid z_{t-1}, u_t) \prod_{t=1}^T p(y_t \mid z_t, u_t)$$

Here $p(z_t | z_{t-1}, u_t)$ is called the transition or dynamics model,

and $p(y_t | z_{t}, u_t)$ is called the observation or emission model.

In both cases, the inputs $u_t$ are optional; furthermore, the

observation model may have auto-regressive dependencies, in which case

we write $p(y_t | z_{t}, u_t, y_{1:t-1})$.

We assume that we see the observations $y_{1:T}$, and want to infer the

hidden states, either using online filtering (i.e., computing

$p(z_t|y_{1:t})$ ) or offline smoothing (i.e., computing

$p(z_t|y_{1:T})$ ). We may also be interested in predicting future

states, $p(z_{t+h}|y_{1:t})$, or future observations,

$p(y_{t+h}|y_{1:t})$, where h is the forecast horizon. (Note that by

using a hidden state to represent the past observations, the model can

have \"infinite\" memory, unlike a standard auto-regressive model.) All

of these computations can be done efficiently using our library, as we

discuss below. In addition, we can estimate the parameters of the

transition and emission models, as we discuss below.

More information can be found in these books:

> - \"Machine Learning: Advanced Topics\", K. Murphy, MIT Press 2023.

> Available at .

> - \"Bayesian Filtering and Smoothing, Second Edition\", S. Särkkä and L. Svensson, Cambridge

> University Press, 2023. Available at

>

## Example usage

Dynamax includes classes for many kinds of SSM. You can use these models

to simulate data, and you can fit the models using standard learning

algorithms like expectation-maximization (EM) and stochastic gradient

descent (SGD). Below we illustrate the high level (object-oriented) API

for the case of an HMM with Gaussian emissions. (See [this

notebook](https://github.com/probml/dynamax/blob/main/docs/notebooks/hmm/gaussian_hmm.ipynb)

for a runnable version of this code.)

```python

import jax.numpy as jnp

import jax.random as jr

import matplotlib.pyplot as plt

from dynamax.hidden_markov_model import GaussianHMM

key1, key2, key3 = jr.split(jr.PRNGKey(0), 3)

num_states = 3

emission_dim = 2

num_timesteps = 1000

# Make a Gaussian HMM and sample data from it

hmm = GaussianHMM(num_states, emission_dim)

true_params, _ = hmm.initialize(key1)

true_states, emissions = hmm.sample(true_params, key2, num_timesteps)

# Make a new Gaussian HMM and fit it with EM

params, props = hmm.initialize(key3, method="kmeans", emissions=emissions)

params, lls = hmm.fit_em(params, props, emissions, num_iters=20)

# Plot the marginal log probs across EM iterations

plt.plot(lls)

plt.xlabel("EM iterations")

plt.ylabel("marginal log prob.")

# Use fitted model for posterior inference

post = hmm.smoother(params, emissions)

print(post.smoothed_probs.shape) # (1000, 3)

```

JAX allows you to easily vectorize these operations with `vmap`.

For example, you can sample and fit to a batch of emissions as shown below.

```python

from functools import partial

from jax import vmap

num_seq = 200

batch_true_states, batch_emissions = \

vmap(partial(hmm.sample, true_params, num_timesteps=num_timesteps))(

jr.split(key2, num_seq))

print(batch_true_states.shape, batch_emissions.shape) # (200,1000) and (200,1000,2)

# Make a new Gaussian HMM and fit it with EM

params, props = hmm.initialize(key3, method="kmeans", emissions=batch_emissions)

params, lls = hmm.fit_em(params, props, batch_emissions, num_iters=20)

```

These examples demonstrate the dynamax models, but we can also call the low-level

inference code directly.

## Contributing

Please see [this page](https://github.com/probml/dynamax/blob/main/CONTRIBUTING.md) for details

on how to contribute.

## About

Core team: Peter Chang, Giles Harper-Donnelly, Aleyna Kara, Xinglong Li, Scott Linderman, Kevin Murphy.

Other contributors: Adrien Corenflos, Elizabeth DuPre, Gerardo Duran-Martin, Colin Schlager, Libby Zhang and other people [listed here](https://github.com/probml/dynamax/graphs/contributors)

MIT License. 2022