https://github.com/unine-chyn/multilstsq

Python 3 module for doing simultaneous linear regression

https://github.com/unine-chyn/multilstsq

abstract-syntax-tree algorithm expression-evaluator linear-regression python-3 python-library python3

Last synced: about 2 months ago

JSON representation

Python 3 module for doing simultaneous linear regression

- Host: GitHub

- URL: https://github.com/unine-chyn/multilstsq

- Owner: UniNE-CHYN

- License: lgpl-3.0

- Created: 2018-03-06T09:05:29.000Z (over 8 years ago)

- Default Branch: master

- Last Pushed: 2018-05-08T14:51:56.000Z (about 8 years ago)

- Last Synced: 2025-03-01T05:17:25.261Z (over 1 year ago)

- Topics: abstract-syntax-tree, algorithm, expression-evaluator, linear-regression, python-3, python-library, python3

- Language: Python

- Homepage:

- Size: 155 KB

- Stars: 1

- Watchers: 3

- Forks: 0

- Open Issues: 0

-

Metadata Files:

- Readme: README.md

- License: LICENSE

Awesome Lists containing this project

README

MultiLstSq

==========

Least squares fitting is a underlying method for numerous applications, the most common one being linear regression. It consists in finding the parameters vector ``β°`` which minimizes ``‖ε‖₂`` in the equation ``y = Xβ + ε``, where `X` is the design matrix, `y` the observation vector, and `ε` the error vector.

Since it is a fundamental algorithm, a number of Python 3 implementations exist, with different feature sets and performance, such as: `numpy.linalg.lstsq`, `scipy.stats.linregress`, `sklearn.linear_model.LinearRegression` and `statsmodel.OLS`.

However, the current available libraries are not designed to work on a large quantity of simultaneous problems, for example solving a least square problem for each pixel of an image. Iterating over a large number of small problems is inefficient. Moreover, when doing linear regression, it is often tedious to build the design matrix `X`.

The goal of `multilstsq` is to work on arrays of problems, with good performance, low memory requirements, reliability and flexibility. It also provides a way to automate the construction of the relevant structures (mostly the design matrix), using a model given as a string. It however does not strive to be a complete statistical library such as what would be provided by `statsmodel` or the language `R`.

To reach these goals, `multilstsq` uses the following techniques:

- It is possible to compute ``β°=(XᵀX)⁻¹Xᵀy`` incrementally, due to the linearity of ``XᵀX`` and ``Xᵀy``, by providing data in chunks.

- Inverting ``XᵀX`` is done by explicit formulas when the dimension is small. This has the advantage of being vector operations which can be applied simultaneously on all problems.

- Masked data are handled as lines of zeros in the design matrix and the observation, which in fact have no effect. This allows adding different amount of data in different subproblems.

- For regression, an expression evaluator is implemented, which converts the input model from the user (for example `b0+b1*x0`) into the complex expression needed to build the design matrix from the vector `X` provided by the user. In that example, it is: `np.concatenate([np.ones(o_dim)[(..., np.newaxis)], ((X)[..., :, 0])[(..., np.newaxis)]])`. This expression evaluator also may be useful for other purposes in other libraries.

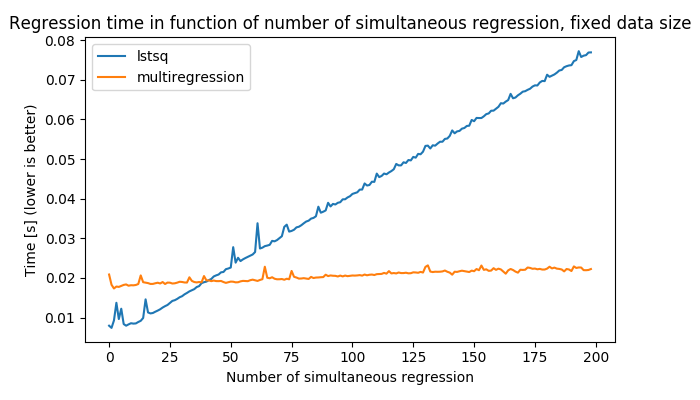

As shown in the following figure, this ensures the algorithm has good performance compared to a loop:

.

Example use

===========

```python

import numpy as np

from multilstsq import MultiRegression

x1 = np.array([1.47, 1.50, 1.52, 1.55, 1.57, 1.60, 1.63, 1.65, 1.68, 1.70, 1.73, 1.75, 1.78, 1.80, 1.83])

y1 = np.array([52.21, 53.12, 54.48, 55.84, 57.20, 58.57, 59.93, 61.29, 63.11, 64.47, 66.28, 68.10, 69.92, 72.19, 74.46])

x2 = np.arange(10)

y2 = np.arange(10)

X = np.ma.masked_all((2, max(len(x1), len(x2)), 1))

y = np.ma.masked_all((2, max(len(x1), len(x2)), 1))

X[0, :len(x1), 0] = x1

X[1, :len(x2), 0] = x2

y[0, :len(y1), 0] = y1

y[1, :len(y2), 0] = y2

mr = MultiRegression((2,), 'b0 + b1*x0 + b2*(x0**2)')

mr.add_data(X,y)

mr.switch_to_variance()

mr.add_data(X,y)

print(mr.beta)

#Identify parameter names in the parameter vector

print(mr.beta_names)

#Get the covariance matrix for the first problem

print(mr.variance[0])

#Get the expression to predict for the first problem

expr = mr.get_expr_for_idx((0,))

#Evaluate at x=1.79

print(expr(1.79))

```

The nice thing about this module is that it is possible to change the model by only changing the line instanciating the MultiRegression object. For example, for a quadratic regression:

```python

mr = MultiRegression((2,), 'b0 + b1*x0 + b2*(x0**2)')

```

Documentation

=============

Documentation is available at http://multilstsq.readthedocs.io/

Contributing

============

Please post issues and pull requests on github. Alternatively, you can also send your patches by email.

The following tools are used to ensure good code quality:

Tool | Status

------------ | -------------

travis-ci | [](https://travis-ci.org/UniNE-CHYN/multilstsq)

AppVeyor | [](https://ci.appveyor.com/project/lfasnacht/multilstsq)

Coveralls | [](https://coveralls.io/github/UniNE-CHYN/multilstsq?branch=master)